Daily

How Parents Can Budget for Back-to-School Season

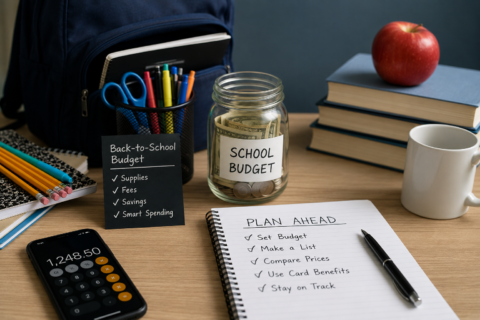

Building a Back-to-School Budget Without Stress Smart planning for school season expenses. Photo by AI....

May 31, 2026

Building a Back-to-School Budget Without Stress Smart planning for school season expenses. Photo by AI....

May 31, 2026

Treasury Bills vs CDs: A Quick Overview In the U.S....

Why Protect Retirement Contributions During a Job Change Matters Switching...

Cosigner Release Explained: Is Refinancing a Better Choice? Choose between...