How Parents Can Budget for Back-to-School Season

Learn how American parents can organize back-to-school expenses without damaging family finances or savings.

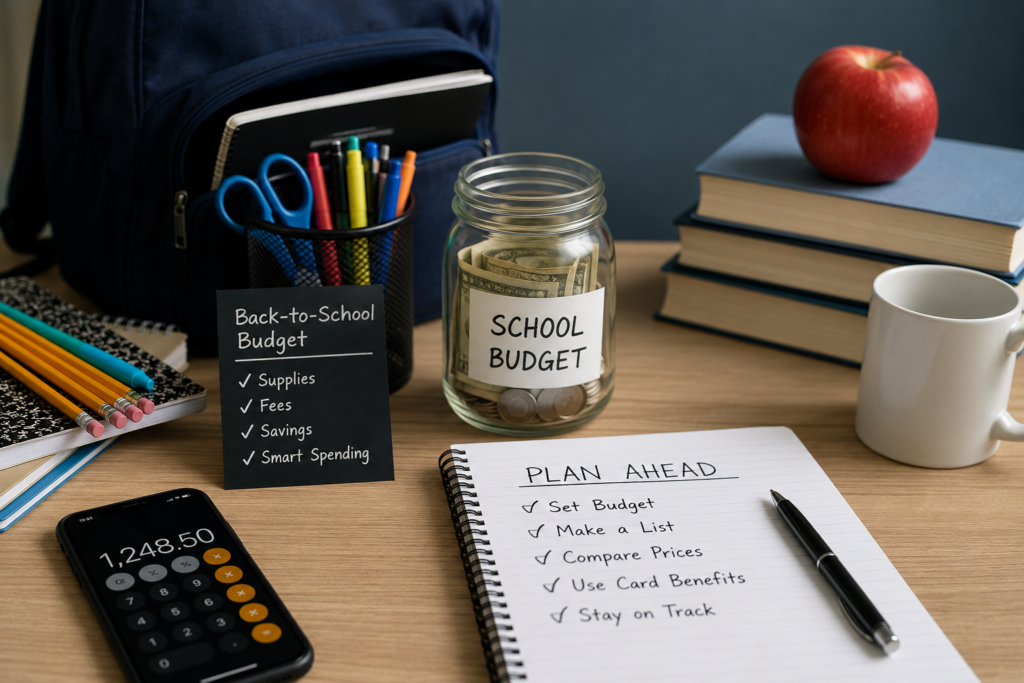

Building a Back-to-School Budget Without Stress

For many American families, back-to-school season no longer feels like a simple yearly routine.

It feels like a second holiday spending season.

Between school supplies, technology, sports fees, clothing, transportation costs, lunch expenses, and activity registrations, parents across the United States are facing a financial cycle that grows more expensive every single year.

According to the National Retail Federation (NRF), American families consistently spend hundreds of billions collectively during back-to-school shopping periods, with average household spending often exceeding $800 per child depending on grade level and technology needs. Rising inflation, elevated transportation costs, and higher consumer prices have pushed school-related spending into territory that many middle-income families now struggle to manage responsibly.

The biggest problem is not necessarily the spending itself. It is the lack of structure around the spending. That is where modern budgeting matters.

🎒 Understanding the Real Cost of Back-to-School Shopping

Back-to-school costs are no longer limited to notebooks and pencils. For many parents in the United States, school preparation now includes:

- laptops & tablets

- software subscriptions

- sports equipment

- extracurricular activity fees

- school transportation

- upgraded internet plans

- uniforms

- classroom contributions

- lunch account funding

The Consumer Price Index data from the U.S. Bureau of Labor Statistics has repeatedly shown inflationary pressure on apparel, electronics, transportation, and household goods over recent years. That directly affects school shopping budgets.

Meanwhile, many families still approach back-to-school season emotionally rather than strategically. That creates unnecessary financial stress.

⚠️ The Biggest Mistake Parents Make

The most common budgeting mistake is treating school spending like isolated purchases instead of a seasonal financial event. Parents often buy:

- supplies one week

- clothes another week

- activity registrations later

- technology upgrades unexpectedly

The result: the household never sees the full spending picture.

This creates what financial analysts call “budget fragmentation.” Individually, the purchases feel manageable. Collectively, they become financially disruptive.

📊 Why Advanced Budgeting Matters More Than Ever

Families with strong financial habits typically approach back-to-school season similarly to how businesses approach quarterly planning. That sounds extreme until you realize the scale of modern household expenses.

A well-structured family budget today must account for:

Ignoring school spending structure often forces families into revolving credit card debt, reduced savings contributions, emergency fund withdrawals, and unnecessary financial stress during fall.

Our view is simple: Back-to-school shopping should never become a debt-driven event. Unfortunately, for millions of Americans, it already has.

💵 Average Back-to-School Expenses in the U.S.

| Category | Estimated Average Cost |

|---|---|

| School supplies | $140–$180 |

| Clothing & shoes | $250–$350 |

| Electronics | $200–$500+ |

| Sports & extracurriculars | $150–$600 |

| Lunch & meal prep | $40–$100 monthly |

| Transportation | Varies significantly |

| Classroom fees | $50–$300 |

For households with multiple children, costs escalate rapidly. And this table does not even include inflation surprises, replacement purchases, seasonal sports expenses, field trips, or unexpected school requests.

Parents who fail to prepare for those “hidden” costs often experience budget breakdowns by October.

💳 Why Credit Card Usage Becomes Dangerous

Back-to-school spending is one of the most common triggers for short-term consumer debt accumulation in the United States. Why? Because the spending feels “necessary.”

Parents rationalize purchases faster during school season because the purchases involve their children. That emotional dynamic weakens spending discipline.

Credit cards can absolutely be useful tools during back-to-school shopping when used correctly (cashback, fraud protection, purchase protection, extended warranties, budgeting organization).

But problems begin when credit cards become:

- emotional financing tools

- instead of payment management tools

That distinction matters enormously.

The “Minimum Payment Trap”

Many younger parents underestimate how aggressively credit card interest compounds. A large school shopping balance carried over multiple months can become significantly more expensive than expected.

- $1,000 at 24% APR Far above original purchase value over time

- $2,500 at 27% APR Can become financially disruptive quickly

The issue is not the purchase itself. The issue is financing routine household expenses with high-interest revolving debt.

Our position is straightforward: If school shopping requires long-term revolving debt, the household budget likely needs structural adjustments — not more available credit.

💻 Why Technology Spending Is Reshaping Budgets

Technology has become one of the largest back-to-school categories in America.

Families mainly bought supplies.

Many students require laptops, tablets, graphing calculators, educational software, cloud subscriptions, and upgraded internet access.

This changes the economics of school preparation completely. According to Pew Research Center findings, digital learning expectations increased significantly after pandemic-era remote learning expansion. Technology is no longer optional in many districts. That means budgeting for education now overlaps with budgeting for consumer electronics.

📱 Smart Families Separate “Need” From “Social Pressure”

One of the most expensive mistakes parents make is confusing educational necessity with social competition. Children today are heavily influenced by TikTok trends, peer pressure, brand culture, and influencer-driven consumption.

Parents feel pressure to upgrade devices constantly, purchase trend-driven products, and overspend on appearance-related items.

But financially stable households usually operate differently. They prioritize:

- functionality

- durability

- long-term value

- realistic educational needs

Not social media aesthetics.

🗂️ A Smarter Back-to-School Budget Framework

Financially organized households often use category-based planning before shopping begins.

- Supplies Fixed amount

- Clothing Fixed amount

- Technology Pre-approved limit

- Activities Planned separately

- Emergency reserve Dedicated backup fund

This prevents emotional overspending during shopping trips. Because once parents enter stores without structure, retailers take control of the decision-making process. And retailers are extremely good at engineered spending environments.

Timing Matters More Than Most Parents Realize

Advanced budgeting is not only about how much you spend. It is also about when you spend. Strategic families:

- monitor seasonal sales cycles

- compare pricing online

- avoid peak-demand panic shopping

- buy durable products during off-season discounts

Late budgeting almost always increases costs. Retailers know desperate parents will pay higher prices close to school start dates. Planning early creates negotiating power.

The Psychological Cost of Disorganized Spending

Financial stress affects parenting quality more than many people admit. Back-to-school financial pressure can contribute to anxiety, household tension, emotional spending, and reduced savings discipline.

Parents often focus only on transaction costs while ignoring stress costs. But stress-driven financial decisions usually create long-term instability. Well-structured budgeting reduces both financial damage and emotional pressure. That matters for the entire household.

🛡️ Emergency Funds Matter During School Season

One overlooked reality: school costs rarely stop after August. Unexpected expenses appear constantly:

- replacement electronics

- sports travel

- fundraiser participation

- school projects

- transportation repairs

- activity uniforms

Parents who fully exhaust available cash during initial shopping often become vulnerable later in the semester. This is why emergency reserves remain critical even during planned spending periods. Using every available dollar for back-to-school shopping is usually a mistake.

✅ What Financially Strong Families Do Differently

Households with long-term financial stability typically:

- 🟢 plan early

- 🟢 set category limits

- 🟢 avoid emotional purchases

- 🟢 separate wants from needs

- 🟢 preserve emergency liquidity

- 🟢 minimize revolving debt

- 🟢 review total seasonal spending afterward

- Most importantly: they treat school spending like a planned financial event — not a shopping emergency. That single mindset shift changes outcomes dramatically.

The Real Goal Is Financial Stability, Not Perfect Shopping

Many parents chase the idea of creating a “perfect” back-to-school season. But financially, perfection is expensive. Children do not need luxury-level school products, trend-driven technology upgrades, or social-media-optimized shopping experiences.

What families actually need is sustainability. Because financially exhausted households enter the holiday season already weakened if back-to-school spending spirals out of control. That creates a dangerous annual cycle: school debt ➔ holiday debt ➔ tax-season recovery ➔ repeat.

Breaking that cycle requires intentional budgeting.

🏁 Final Thoughts

Back-to-school season in the United States has evolved into one of the largest annual household spending events. And for many parents, the challenge is no longer simply affording supplies. The challenge is managing a growing ecosystem of recurring educational expenses without damaging long-term financial stability.

Smart budgeting today requires more than simple cost-cutting. It requires planning, structure, emotional discipline, category management, and realistic expectations.

Parents who approach school spending strategically gain something far more valuable than temporary savings: They gain financial control. And in an economy where household expenses continue rising faster than many incomes, control matters more than ever.

Related content

Treasury Bills vs CDs: Which Is Better?

Compare Treasury Bills vs CDs to find the best safe short-term investment option for yield, liquidity, and tax efficiency.

Keep reading * You will remain on the current website