How to Build a Tax Refund Plan Before the Money Arrives

Build a smart tax refund plan before it arrives. Pay off debt, invest strategically, and strengthen your financial future in the U.S.

Learn the Way to Use Your Tax Refund to Your Advantage

In the United States, many people treat their tax refund as an “annual bonus.”

In 2025, the average refund from the Internal Revenue Service was around $3,400 — enough to meaningfully change someone’s financial trajectory for the entire year.

And yet, most people waste that money.

Not because they don’t earn enough. But because they lack a strategy.

If you want to use your tax refund as a real financial growth tool — not just temporary relief — planning needs to start before the money arrives.

The Most Common Mistake: Planning After You Receive It

Once the money hits your account, your decision-making changes.

You’re no longer planning, you’re reacting.

That leads to three common behaviors:

- Impulse spending (“I deserve this”)

- Poorly structured debt payments

- Consumption disguised as investing

Simple rule:

If you haven’t decided where the money goes before you receive it, it’s already mentally spent.

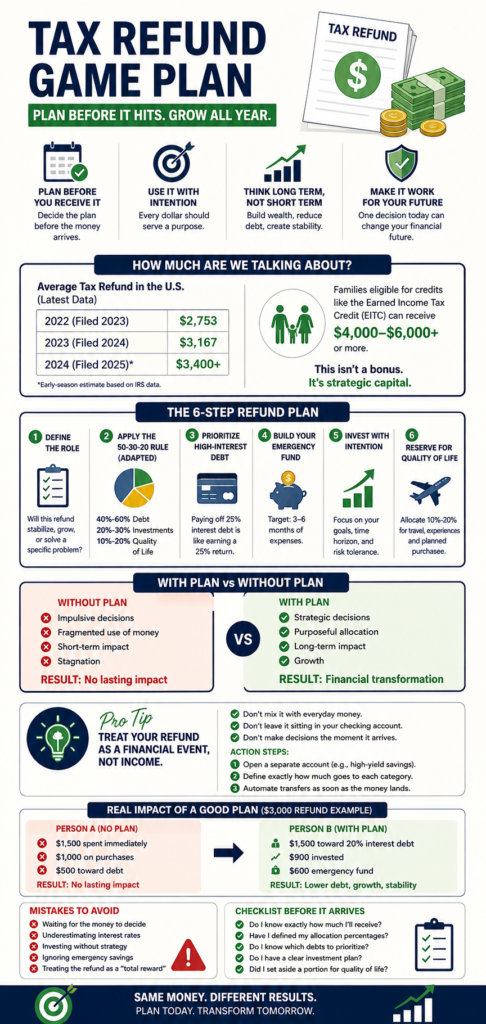

How Much Money Are We Talking About (Updated U.S. Data)

According to the latest data from the Internal Revenue Service:

| Tax Season (Filed Year) | Average Refund |

|---|---|

| 2022 (filed 2023) | ~$2,753 |

| 2023 (filed 2024) | ~$3,167 |

| 2024 (filed 2025)* | ~$3,400+ |

*Early-season estimate based on IRS processing data.

For families eligible for credits like the Earned Income Tax Credit, refunds can be significantly higher, often exceeding $4,000–$6,000 depending on income and dependents.

What this actually means:

- This isn’t small money.

- It’s not a bonus.

- It’s strategic capital that most people mismanage.

What Separates Those Who Grow from Those Who Stay Stuck

The difference isn’t the size of the refund.

It’s the decision-making system.

People who make financial progress:

- Plan ahead

- Allocate with intention

- Think in terms of long-term impact

People who stay stuck:

- Wait for the money to arrive

- Decide emotionally

- Focus only on the short term

How to Build a Plan Before the Money Arrives

Here’s a direct framework, no unnecessary theory.

1. Define the Role of Your Tax Refund

Before thinking about numbers, answer this:

What is this money for?

- Stabilizing your finances?

- Accelerating growth?

- Solving a specific problem?

Without this clarity, you’re just dividing money, not building a strategy.

2. Use the 50-30-20 Rule (Adapted for Refunds)

Unlike a monthly budget, this requires a more aggressive approach.

Recommended structure:

| Category | Percentage | Goal |

|---|---|---|

| Debt | 40%–60% | Reduce interest and pressure |

| Investments | 20%–30% | Build wealth |

| Lifestyle | 10%–20% | Avoid rebound spending |

3. Prioritize High-Interest Debt

In the U.S., the problem isn’t debt. It’s compound interest working against you.

Typical example:

| Debt Type | Average Rate |

|---|---|

| Credit cards | 20%–25% |

| Personal loans | 10%–15% |

| Auto loans | 6%–9% |

Key insight:

Paying off a 25% debt is equivalent to earning a guaranteed 25% return.

There is no traditional investment that matches that level of safety and return.

4. Build (or Strengthen) Your Emergency Fund

If you don’t have at least 3 months of expenses saved, your financial plan is fragile.

Your tax refund is one of the fastest ways to fix that.

Recommended target:

- Minimum: 3 months

- Ideal: 6 months

See tips to build a long-term investment portfolio.

5. Invest with Intention — Not Impulse

Investing isn’t about putting money anywhere.

In the U.S., common options include:

- 401(k)

- Roth IRA

- Brokerage accounts

The mistake? Investing without a clear goal.

Ask yourself:

- Does this investment have a time horizon?

- Is it for retirement or liquidity?

- Does it match my risk tolerance?

6. Reserve a Portion for Quality of Life

This may seem counterintuitive, but it’s necessary.

If you allocate 100% of your refund “rationally,” there’s a real risk:

You compensate emotionally later and overspend throughout the year.

That’s why you should reserve 10%–20% for:

- Travel

- Experiences

- Planned purchases

This keeps your system sustainable.

Practical Comparison: With vs Without a Plan

| Aspect | No Plan | With Plan |

|---|---|---|

| Decision-making | Impulsive | Strategic |

| Money usage | Fragmented | Intentional |

| Financial impact | Short-term | Long-term |

| Final outcome | Stagnation | Growth |

The “Pro Tip” (Your Real Edge)

Here’s what almost no one does:

Treat your tax refund as a financial event, not income.

What that means:

- Don’t mix it with everyday money

- Don’t leave it sitting in your checking account

- Don’t make decisions the moment it arrives

Action steps:

Before the deposit:

- Open a separate account (e.g., high-yield savings)

- Define exact allocation percentages

- Automate transfers as soon as the money arrives

This eliminates 90% of emotional decisions.

The Real Impact (In Numbers)

Let’s compare two people receiving a $3,000 refund:

Person A (No Plan):

- $1,500 spent immediately

- $1,000 on purchases

- $500 toward debt

Result: no lasting impact

Person B (With a Plan):

- $1,500 toward 20% debt

- $900 invested

- $600 emergency fund

Result:

- Interest savings

- Wealth growth

- Financial stability

Same amount. Completely different outcome.

Mistakes to Avoid

See the main mistakes to avoid when planning your tax refund in advance.

- Waiting until the money arrives

- Underestimating interest rates

- Investing without strategy

- Ignoring emergency savings

- Treating the refund as a full reward

Checklist Before Your Refund Arrives

See the checklist to plan your tax refund before the money arrives.

- Do I know exactly how much I’ll receive?

- Have I defined allocation percentages?

- Do I know which debts to prioritize?

- Do I have a clear investment plan?

- Did I reserve something for lifestyle?

If any answer is “no,” your plan isn’t ready.

Image to save on your phone

See a complete and practical guide to planning your finances with your tax refund.

Conclusion: Your Tax Refund Can Change Your Year

Most people treat their tax refund as temporary relief.

Few treat it as leverage.

And that’s where the difference lies.

You don’t need to earn more to improve your finances.

You need to make better decisions with the money you already receive.

If you structure your tax refund before it arrives, you:

- Pay off debt faster

- Build wealth

- Gain financial control

In the end, it’s not about the amount. It’s about the system. And those who build systems grow.

FAQ: Tax Refund Planning in the U.S.

Related content

Statement Date vs. Due Date

Understand the difference between Statement Date and Due Date, how they affect your credit card, and how to use them to your advantage daily.

Keep reading * You will remain on the current website